Förra året tog Gartner bort 14 molnleverantörer från sin Magic Quadrant för Cloud IaaS och valde att endast fokusera på globala leverantörer som för närvarande erbjuder, eller utvecklar, integrerade IaaS- och PaaS-erbjudanden i hyperscale. Denna lilla vårstädning resulterade i en mer hanterbar lista med sex företag som klassificerades i två distinkta segment: ledarna, som består av Amazon Web Services, Microsoft och Google, och nischaktörerna, som representeras av Alibaba, Oracle och IBM.

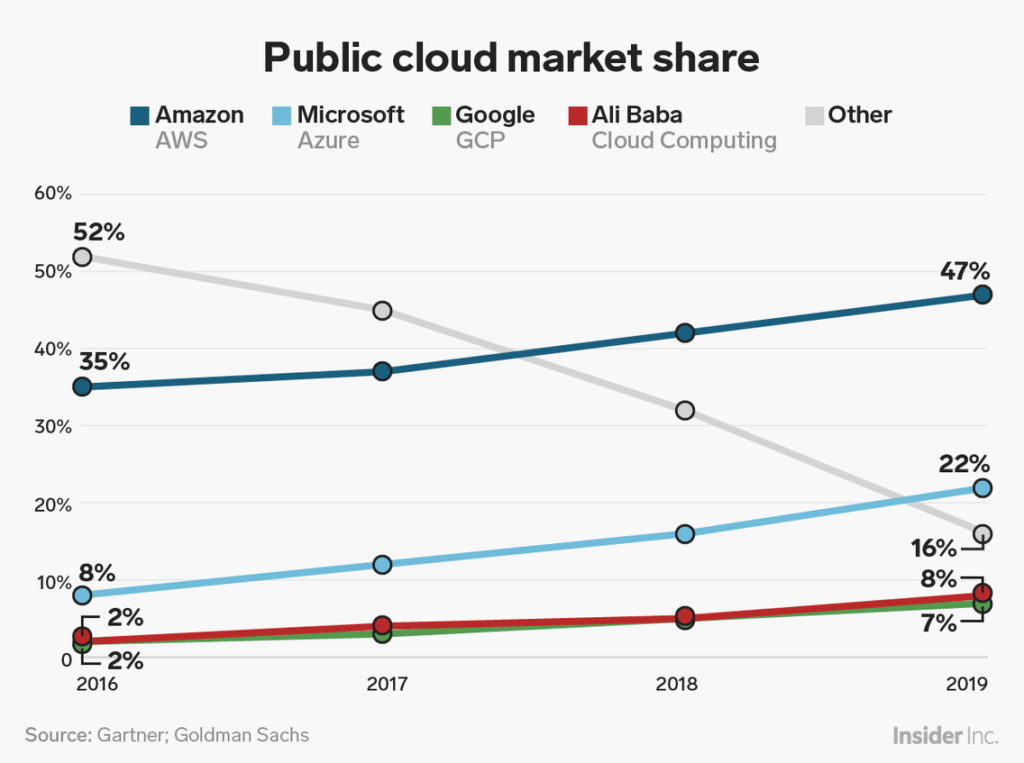

Även inom denna förenklade ligatabell med tre aktörer fortsätter Amazon att vara den klara ledaren när det gäller intäkter och marknadsandelar.

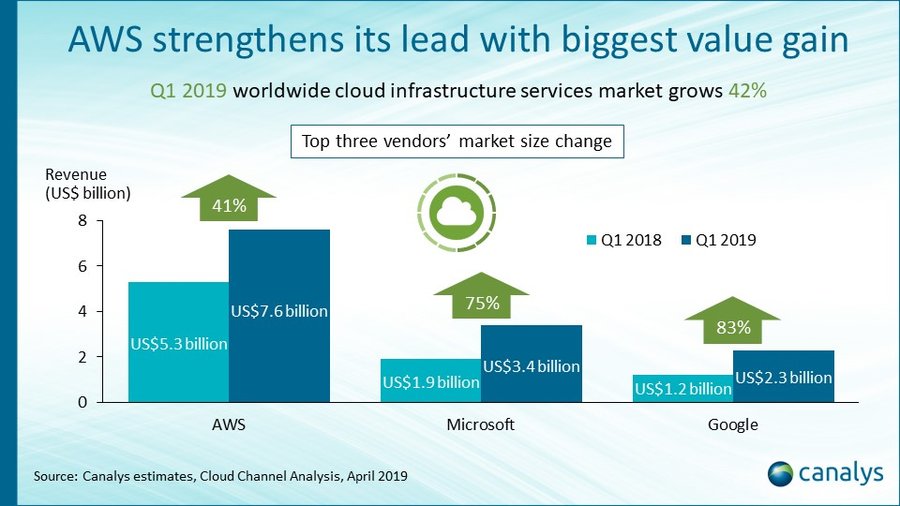

Nu dominerar visserligen AWS molnmarknaden, men Microsoft och Google växer mycket snabbare.

Enligt siffrorna för Q1 2019 växer dessa utmanare med 75 respektive 83 procent, vilket kan jämföras med en tillväxt på 41 procent för AWS.

AWS marknadsandel har också stagnerat på 33 procent mellan Q1 2018 och 2019.

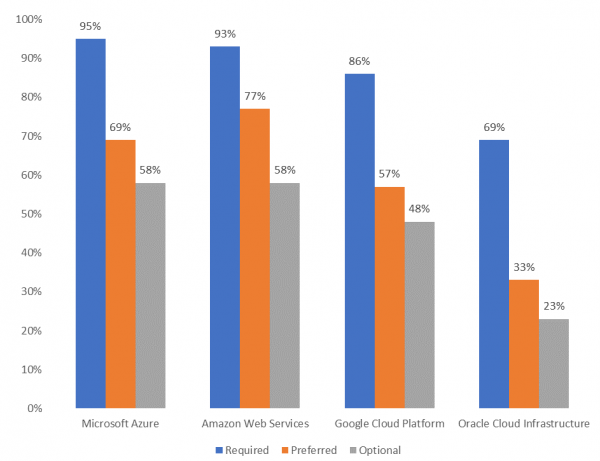

Dessutom visar Gartners scorecard, som utvärderar leverantörer av offentliga IaaS-moln utifrån 263 obligatoriska, föredragna och valfria kriterier, att Azure har dragit ifrån AWS när det gäller obligatoriska kriterier för första gången sedan poängbedömningen inleddes.

Satsa på multicloud och hybrid

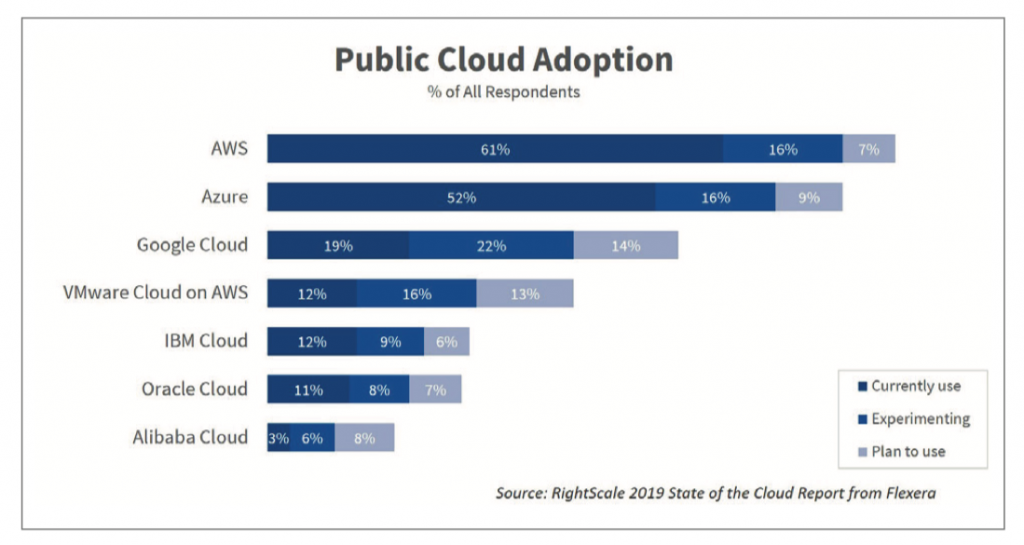

Men även om marknaden för IaaS-moln smälter samman till en jämförelse mellan ”de tre stora och andra”, visade RightScales undersökning 2019 State of the Cloud att företag kombinerar offentliga och privata moln i en hybridstrategi med flera moln som i genomsnitt utnyttjar nästan fem moln.

En annan studie från Kentik visade att den vanligaste molnkombinationen var AWS och Azure, med kombinationen AWS-Google Cloud inte långt efter.

Även om offentliga moln fortfarande är högsta prioritet för företag, ökar antalet företag som använder en hybridstrategi med offentliga och privata moln.

Samtidigt har antalet företag med en multicloud-strategi, som kombinerar flera offentliga eller privata moln, minskat.

Allt detta tyder på att molnmarknaden inte är ett nollsummespel. Företagen använder en kombination av molnleverantörer, inklusive nischaktörer, för att utforma lösningar som ger de bästa resultaten. Och molnleverantörerna måste ta hänsyn till denna preferens för hybridmoln när de utvecklar lösningar för sina kunder.

Ännu viktigare är att inget av detta gör det lättare för kunderna att välja rätt leverantörer för sina arbetsbelastningar eftersom det saknas ett gemensamt ramverk för bedömning. Men det är möjligt att definiera en mall med några viktiga överväganden som bör ligga till grund för valet av molnleverantör.

Välja leverantör av molntjänster

Det finns flera faktorer som kan påverka ett företags val av molnleverantör, bland annat plattformens val av teknik och arkitektur, datasäkerhet, efterlevnad och styrningspolicy, interoperabilitet, portabilitet och migrationsstöd, färdplan för utveckling av tjänster etc.

Cloud Industry Forum, en brittisk icke vinstdrivande organisation som främjar molntjänster, har en ganska omfattande lista med 8 kriterier för att välja rätt molntjänstleverantör. På Vinnter anser vi att det finns fyra viktiga aspekter vid valet av molnleverantör:

Närhet till platsen: Det finns två skäl att säkerställa att molntjänstleverantörer har faktisk verksamhet på kundens målmarknad. Den första är latensen, som vissa till och med har kallat för akilleshälen när det gäller molntjänster.

En studie av den globala nätverksprestandan hos AWS, Google Cloud och Microsoft Azure visade att datacentrets placering direkt påverkade nätverkslatensen och att nätverksprestandan varierade mellan olika tjänsteleverantörer när man anslöt till olika regioner.

Denna fördröjning kan få enorma konsekvenser för prestandan i många moderna affärs- och IoT-applikationer som är beroende av och förväntar sig låg latens.

Den andra kritiska faktorn är datasuveränitet. Många länder, däribland Ryssland, Kina, Tyskland, Frankrike, Indonesien och Vietnam, har regler om dataregistrering som kräver att data lagras i regionen. GDPR:s suveränitetskrav innebär strikta mandat för insamling och behandling av EU-medborgares uppgifter.

Molnleverantörerna svarar på dessa krav på latens och suveränitet genom att öppna flera regionala datacenter. Till exempel tillkännagav AWS planer på att öppna en infrastrukturregion i Italien, företagets sjätte i Europa, som skulle uppfylla kraven på både låg latens och dataresidens.

I Tyskland har Microsoft placerat kunddata i sina datacenter hos en oberoende tysk dataförvaltare, vilket gör det svårt för någon, inklusive Microsoft eller amerikanska myndigheter, att få tillgång till dem utan kundens tillstånd.

Transparent prissättning: Att optimera molnkostnaderna fortsätter att vara en topprioritet, även bland avancerade molnanvändare, och en studie uppskattar slöseriet till cirka 35 procent av molnutgifterna.

Studien identifierade också fyra orsaker till detta slöseri: komplexiteten i molnprissättningen, en bättre-säker-än-sorry-strategi som leder till överprovisionering, brist på insyn i kostnadskonsekvenser och brist på lämpliga verktyg för att optimera utgifterna.

I takt med att molnleverantörerna lanserar nya innovationer och prismodeller förväntas prissättningen bara bli mer komplicerad utan någon grund för jämförelse mellan olika tjänster.

Faktum är att 2018 förutspåddes bli det år då molnleverantörerna skulle konsolidera och förenkla sina erbjudanden och prisstrukturer.

En transparent prissättningsmodell kan hantera nästan alla de slöserifaktorer som nämnts tidigare. Det ger kunderna en gemensam och objektiv grund för att jämföra och välja den tjänst som bäst passar deras arbetsbelastning samt optimera tillhandahållandet till den faktiska efterfrågan.

Tillgänglig dokumentation och support: Dokumentation och kundsupport är kritiska faktorer, ofta skillnaden mellan produktivitet och slöseri, inom ett utvecklingsområde som cloud computing. Omfattande och tillgänglig dokumentation kan göra det lättare för kunderna att implementera och hantera sina molntjänster på ett mer optimalt sätt. Detta måste backas upp av 24/7 kundservice och dedikerade account managers som hjälper kunderna att lösa sina molntjänstproblem och förfrågningar.

Både Google Cloud och AWS ger tillgång till omfattande dokumentation samt forum där kunderna kan ta upp frågor om implementering eller prestanda. Alla de tre största leverantörerna erbjuder en lägre supportnivå som standard, men förväntar sig att kunderna ska betala för något mer. Till exempel erbjuder Google och AWS olika nivåer av support till olika priser.

Framöver kan den dokumentation och support som erbjuds av en molntjänstleverantör bli en viktig särskiljande faktor i kundernas val av molnplattform.

Hitta rätt kompetens för molnet: I takt med att allt fler företag flyttar sina arbetsbelastningar till molnet ökar efterfrågan på personer som har kompetens att utveckla, driva och underhålla slutanvändartjänster som används i en molnmiljö. Detta kommer att vara en kritisk faktor oavsett val av molntjänstleverantör.

Men att skaffa rätt kompetens inom molntjänster har enligt uppgift blivit en riktig kris, och en betydande majoritet av IT-cheferna anser att det är ”ganska svårt” att hitta talanger inom molntjänster.

För att hantera denna kris rekommenderar Deloitte företag att börja med en inventering av företagets kompetens inom cloud computing på olika områden som arkitektur, säkerhet, styrning, drift och DevOps samt kompetens som är specifik för molnvarumärken.

Nästa steg är att definiera vilka färdigheter inom dessa områden som krävs för att företaget ska nå dit det vill när det gäller molnteknik. Slutligen, utbilda, anställ och/eller ersätt talanger för att bygga upp en molnbaserad strategi för teknik.

Idag är det helt enkelt inte möjligt att skapa en jämförelsemall för alla större tjänsteleverantörer som skulle vara relevant för alla företag som vill välja en molnplattform. Men det finns vissa bredare teman som gäller för alla tjänster och som måste beaktas för att avgöra vad som passar bäst för varje företags teknik och arbetsbelastningsprofil, användningsmönster, tekniska mognad och budget.

Ännu viktigare är att molnet inte är den plug-and-play-miljö som det utlovades att vara. Även efter införandet kommer alla företag att behöva intern molnkompetens för att påskynda utveckling och innovation. Det kommer kanske att bli den största utmaningen av alla.